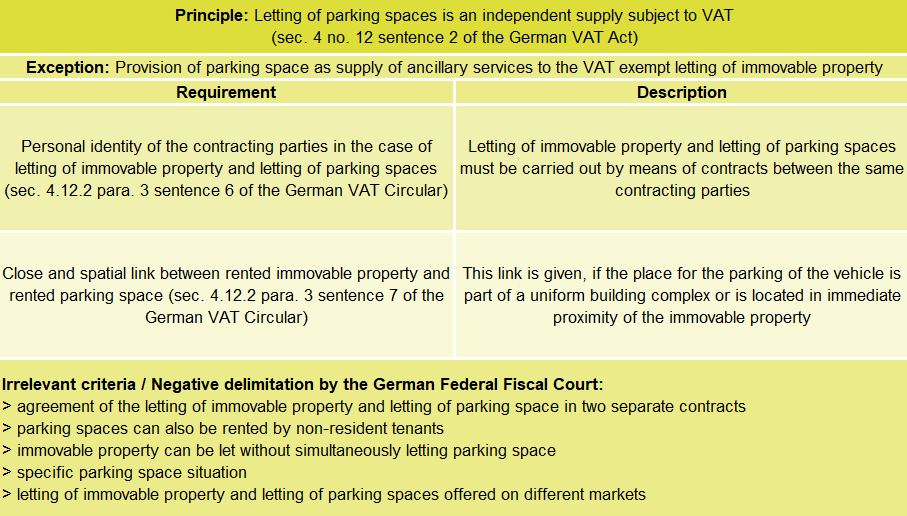

1 Introduction

In its judgment of 10 December 2020, the 5th Senate of the German Federal Fiscal Court (V R 41/19) overturned the previous judgment of the Tax Court Thuringia of 27 June 2019 (3 K 246/19; see KMLZ Newsletter 04 | 2020) on the taxable letting of parking spaces to residential tenants and dismissed the legal action in its entirety. The Federal Fiscal Court thus continues to expand on its jurisprudence in this regard, according to which the letting of parking spaces can be deemed a supply of ancillary services to the VAT exempt letting of immovable property. This is also in line with the previous opinion of the tax authorities.

2 Facts

Between 2011 and 2014, the plaintiff was engaged in the construction of a building complex, which he ultimately intended to rent out subject to VAT. Therefore, the plaintiff fully deducted the input VAT from the construction of the building in 2012 and 2013. The building complex consisted of a front and a rear building with rental home units and an intermediate complex that served as a connection unit in which, among other things, the parking spaces in dispute were located. It was possible to access the intermediate complex by way of the parking spaces directly, independently of the front and rear buildings’ access points. The parking spaces were rented to the residential tenants, as well as to third parties.

As from 2014, the plaintiff decided to rent some of the units for permanent residential purposes and thus VAT exempt. In the process, some of the underground parking spaces located in the intermediate complex were rented to the permanent residential tenants. The plaintiff treated this letting of parking spaces as an independent supply subject to VAT. Within the scope of a special VAT audit, the tax office assessed the letting of parking spaces to tenants who were, at the same time, residential tenants, to be ancillary services to the VAT exempt letting of living space and adjusted the corresponding input VAT deduction from the construction of those parking spaces. Following an unsuccessful appeal, the Tax Court Thuringia upheld the subsequent legal action and justified its judgment on the grounds that the required close and spatial link between the supplies of services in question did not exist in the case in question and therefore there was no uniform supply of services in the form of main and ancillary supply. The tax authorities’ corresponding correction was therefore unlawful. The German Federal Fiscal Court, however, did not follow this opinion and thus confirmed its previous opinion.

3 German Federal Fiscal Court decision

The German Federal Fiscal Court overturned the judgment of the Tax Court Thuringia and dismissed the legal action in its entirety. The Fiscal Court of Thuringia had failed to recognise that the close and spatial link between the letting of living space and the letting of parking spaces is also to be affirmed in cases where the parking space is located in underground garages in an intermediate complex and thus outside the residential buildings themselves. It was irrelevant that the parking spaces were also rented by external non-resident tenants and that they could reach the parking spaces without the need to enter the front or rear residential buildings. In addition, it was irrelevant that the living space could also be rented without simultaneously letting a parking space. Furthermore, the specific parking space situation and the fact that the letting of parking space and living space was offered on different markets were irrelevant.

4 Consequences

With this judgment, the German Federal Fiscal Court confirms its previous jurisprudence on the VAT treatment of the letting of parking spaces in the case of simultaneous letting of living space to the same residential tenant. As a result, the German Federal Fiscal Court has established various criteria that are irrelevant for the assumption of a supply of ancillary services to the VAT exempt residential space rental.

It remains to be seen as to what extent the German Federal Fiscal Court will extend the line as regards the close and spatial link between the letting of living space and letting of parking spaces beyond the individual case at issue. The criteria mentioned in the judgment suggest a broad interpretation. Thus, depending on the individual case, landlords must also assume a uniform VAT exempt supply of rental services if the parking space is not located in the immediate building complex, but the tenant need only walk a few metres within a few minutes in order to arrive at his parking space.

Contact:

Dr. Jochen Tillmanns

Lawyer, Dipl.-Finanzwirt (FH)

Phone: +49 211 54095381

E-Mail: jochen.tillmanns@kmlz.de

As per: 28.06.2021