1 Background

If a recipient of a supply has paid too much VAT to a supplier (on the basis of an invoice issued showing unduly charged VAT according to sec. 14c of the German VAT Act), he must, in principle, seek to recover this amount from the supplier under civil law. However, if it is impossible or excessively difficult for the recipient to enforce this civil law claim, he may have a direct claim against his tax office for payment of this VAT amount - the so-called Reemtsma claim. The ECJ previously set out the principles of such a claim in its Reemtsma decision (judgment of 15 March 2007 – C 35/04). However the details pertaining to making a Reemtsma claim have been disputed ever since. In its circular of 12 April 2022, the Federal Ministry of Finance took a very restrictive view (KMLZ VAT Newsletter 20 | 2022). According to this, the Reemtsma claim should not apply if, inter alia, the recipient’s civil law claim against the supplier is time-barred under civil law. The Fiscal Court of Münster subsequently referred this strict view to the ECJ for a decision (KMLZ VAT Newsletter 33 | 2022).

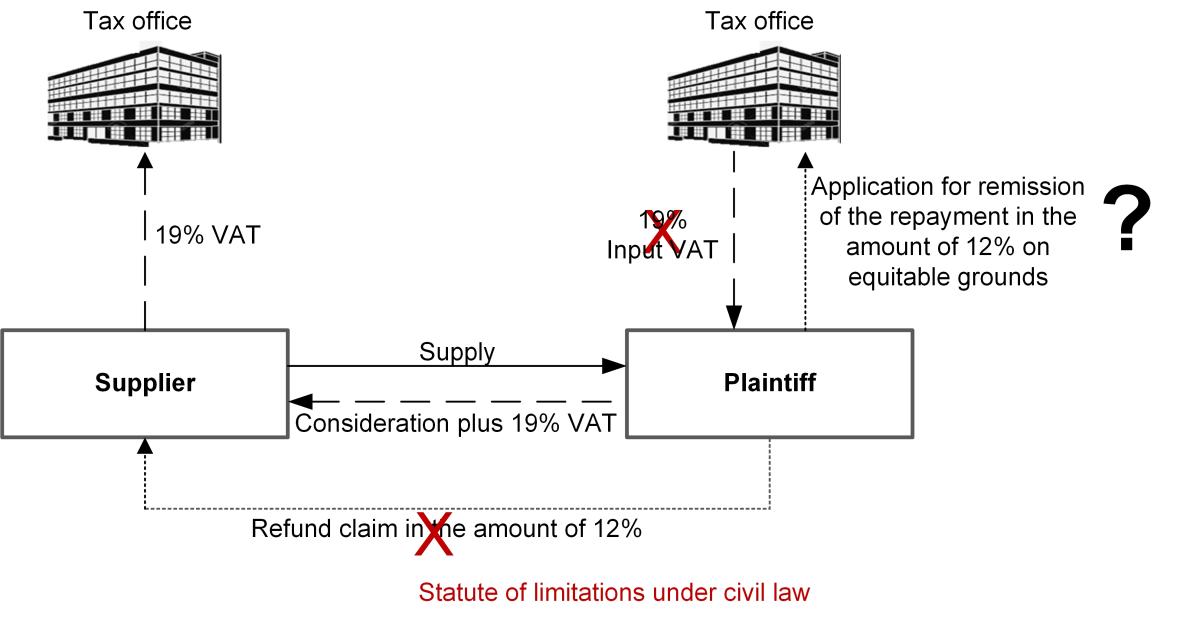

2 Facts

The plaintiff is engaged in the commercial timber trade. He purchased timber at the standard VAT rate (19%) and resold it at the reduced VAT rate (7%). The suppliers paid the 19% VAT to the tax authorities. The tax office denied the plaintiff’s input VAT deduction in the amount of the difference between the standard and reduced VAT rates (12%). When the plaintiff attempted to take recourse against his suppliers for the difference, they invoked the statute of limitations under civil law. The plaintiff subsequently filed an application for a grace decision with his tax office for a refund of the corresponding VAT amount in accordance with the Reemtsma principles, plus interest. After the tax office rejected the application, the plaintiff addressed the Fiscal Court of Münster. The latter referred several questions to the ECJ:

- Can the recipient make a Reemtsma claim even if the supplier is still able to correct the invoices in accordance with sec. 14c of the German VAT Act? In the opinion of the Fiscal Court of Münster, there would be a risk that the tax authorities could potentially, and to their obvious detriment, reimburse the VAT twice.

- Does the Reemtsma claim exist even if the recipient’s civil law claim against the supplier is time-barred?

- Does the Reemtsma claim also include interest?

3 ECJ decision

The ECJ first states in its judgment of 7 September 2023 in the case Schütte (C-453/22) that the Reemtsma claim exists even if recourse under civil law is time-barred. The ECJ goes even further: according to the ECJ, the statute of limitations constitutes a reason for making the enforcement of the civil law claim excessively difficult. The recipient can also assert the Reemtsma claim if the supplier could theoretically still make a correction pursuant to sec. 14c of the German VAT Act. If the supplier invokes the statute of limitations under civil law vis-à-vis the recipient, it is acting improperly if it also requests a refund after having made a correction according to sec. 14c of the German VAT Act. The tax office can refuse payment to the supplier. Therefore, there is no de facto risk of a double reimbursement at the expense of the tax authorities. The Reemtsma claim is also subject to interest based on the principle of fiscal neutrality. The ECJ has repeatedly ruled that the tax authorities do not only have to reimburse the taxable person for the wrongly levied VAT but must also compensate the recipient for any liquidity disadvantage he has suffered.

4 Consequences for the practice

The Reemtsma claim therefore also applies in the case of civil law limitation. This is consistent. The recipient thus experiences further protection if his claim to deduct input VAT has failed. The contrary view of the Federal Ministry of Finance (circular dated 12 April 2022; KMLZ VAT Newsletter 20 | 2022) therefore violates EU law and must be abandoned. This should also apply to other passages of the Federal Ministry of Finance’s letter that fall short of the ECJ's standards. Further questions regarding the Reemtsma claim are already before the ECJ, awaiting clarification (C-83/23). The German Federal Fiscal Court has referred further questions to the ECJ for decision in a cross-border case. One of the questions to be clarified is how the Reemtsma claim should be handled if the tax office has already unlawfully refunded the VAT, according to sec. 14c of the German VAT Act, to the supplier. Affected recipients should apply for a grace decision and appeal. Proceeding against the strict view of the tax authorities now appears promising in many cases.

Contact:

Dr. Thomas Streit, LL.M. Eur.

Lawyer

Phone: +49 89 217501275

thomas.streit@kmlz.de

As per: 13.09.2023