1 Background

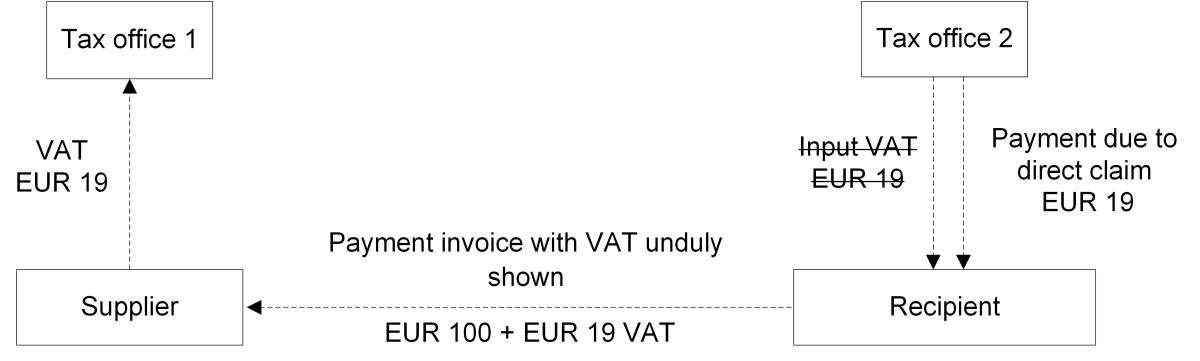

The direct claim or so-called “Reemtsma claim” was introduced by the ECJ in 2007 (judgment of 15 March 2007 - C-35/05). What is this claim about? A recipient of a supply receives an invoice, showing VAT, and pays this amount to the supplier. He then claims input VAT deduction. The competent tax office, however, denies the recipient his input VAT deduction, (either from the outset or retrospectively), based on the fact that the VAT is unduly shown in the invoice (sec. 14c of the German VAT Act). If the recipient wants to reclaim the VAT amount paid, he has to claim it back from the supplier under civil law - if need be, by involving the civil courts. However, if the civil law claim is unenforceable or is excessively difficult (e.g. in the case of the insolvency of the supplier), the ECJ grants the recipient a so-called direct claim against his competent tax office. In financial terms, this claim corresponds to input VAT deduction.

2 Federal Ministry of Finance’s letter: core content and evaluation

In its letter of 12 April 2022, the Federal Ministry of Finance recognises the Reemtsma claim for the first time, but simultaneously considerably reduces the claim’s scope of application:

- The recipient must file his Reemtsma claim with his competent tax office by means of a separate application for equitable relief in accordance with secs. 163, 227 of the German Fiscal Code.

Note: This is likely to be contrary to Union law: As regards the Reemtsma claim, the tax office is not entitled to exercise any scope of discretion. Moreover, the need for separate proceedings contradicts the principle of procedural economy.

- The Ministry of Finance wants to take into account any contributory negligence on the part of the recipient in the preparation of the incorrect invoice.

Note: The ECJ has not yet imposed such a restriction.

- As a rule, the recipient must first reclaim the unduly paid amount from the supplier through civil law. The VAT adjustment procedure according to sec. 14c para. 1 German VAT Act, takes precedence over the Reemtsma claim. The civil law claim is regularly only deemed impossible or excessively difficult if an application for insolvency proceedings against the supplier has been rejected because the value of the debtor’s assets are inadequate to cover the costs of the insolvency proceedings. In the case of ongoing insolvency proceedings it is necessary to wait until the insolvency proceedings are concluded.

Note: Even in the run-up to insolvency proceedings, it is excessively difficult for the recipient to assert his claim.

- The Reemtsma claim is accessory to the civil law claim. In the case of a gross price agreement, it is excluded. If the civil law claim is no longer enforceable due to the statute of limitations (e.g. pursuant to sec. 195 of the German Civil Code), the same applies to the Reemtsma claim.

Note: On the one hand, the German Federal Court of Justice sometimes recognises a claim for recovery even in the case of a gross price agreement. On the other hand, the Reemtsma claim is precisely intended for use in the case of unenforceability of the civil law claim. Consequently, the statute of limitations should be irrelevant.

- The Reemtsma claim is excluded if no supply has been rendered (sec. 14c para. 2 of the German VAT Act).

Note: The ECJ has not yet imposed such a restriction.

- The other requirements for input VAT deduction must also be met (e.g. procurement of goods or services for the company, proper invoice).

Note: The ECJ has not yet imposed such a restriction.

- The Reemtsma claim requires that the tax authorities have been enriched. The legal basis for the claim therefore does not exist if the supplier has not paid the VAT to the tax office or the tax office has refunded the VAT to the supplier (at least if this was justified).

Note: In the case of input VAT deduction - the conditions of which the Ministry of Finance transfers to the Reemtsma claim - the receipt of the VAT amount by the tax authorities is irrelevant.

3 Conclusion

It is to be welcomed that the Ministry of Finance is recognising the Reemtsma claim, albeit approx. 15 years late. However, on the negative side is the fact that the Ministry of Finance has excessively restricted this claim. The claim, which is to serve the purpose of maintaining the neutrality of VAT, will not, in many cases, achieve this objective. Many of the restrictions imposed by the Ministry cannot be derived from the ECJ’s jurisprudence and, in reality, are actually likely to contradict the principles of EU law. Progressive tax judges will be increasingly called upon to examine the Ministry of Finance’s restrictions from an EU law perspective and, if need be, refer them to the ECJ for clarification with regard to EU law.

Contact:

Dr. Thomas Streit, LL.M. Eur.

Lawyer

Phone: +49 89 217501275

thomas.streit@kmlz.de

As per: 05.05.2022