1 Facts, Federal Fiscal Court, judgment of 23.10.2019 – XI R 18/17

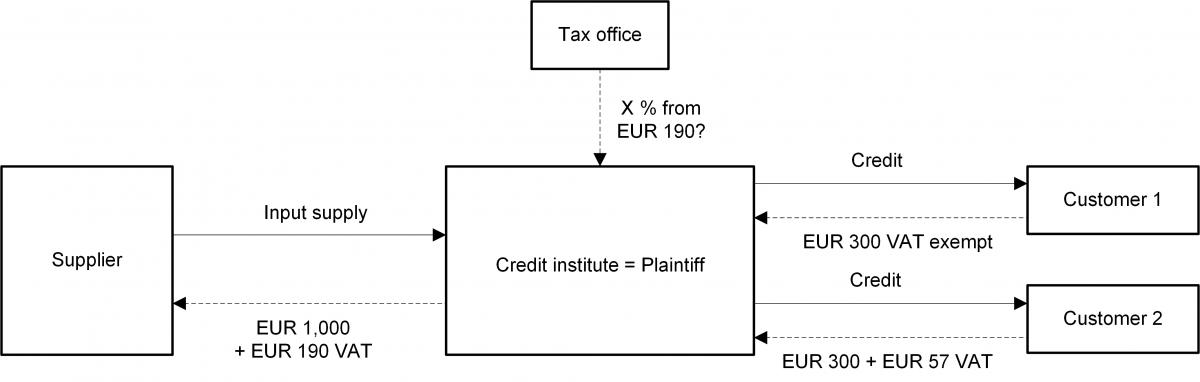

The Plaintiff is a credit institution which used input supplies for both taxable and VAT exempt granting of credits. It applied the so-called Philipowski method to determine the required deductible proportion of input VAT. This method combines the turnover-based allocation key with a personnel requirements calculation. As a result, the Plaintiff calculated a higher deductible proportion of input VAT than the tax office intended to grant. The tax office used a turnover-based allocation key that took the Plaintiff’s own investments into account. In addition, the tax office wanted to apply a separate allocation key for a certain group of input supplies (supply of IT services).

2 Reasons for the decision

The Federal Fiscal Court based its decision on the general principles for determining the deductible proportion of input VAT. According to these principles, a taxable person can – as provided for by German law – make an estimate deviating from the turnover-based allocation key. However, the estimate must be appropriate. It must represent a more precise method for determining the deductible proportion of input VAT than the turnover-base allocation key. However, it need not be the most precise method available.

The Federal Fiscal Court classified the Philipowski method as “not appropriate”. The Court considered itself bound by the opinion of the preceding Tax Court of Munich, which found that a large number of the Plaintiff’s employees were not taken into account in the personnel requirements calculation, even though they contributed to the Plaintiff’s operating result. In doing so these said employees used input services, which were subject to VAT. Consequently, they were required to be included in the calculation. Furthermore, the Tax Court of Munich considered the combination of the turnover-based allocation key and the personnel requirements calculation as not being appropriate. The Federal Fiscal Court did not comment on this last point. The Federal Fiscal Court considered it appropriate to calculate the deductible proportion of input VAT on the basis of a turnover-based allocation key. However, the Federal Fiscal Court confirmed the Munich Tax Court’s approach in also applying this turnover-based allocation key to the supply of IT services.

3 Consequences for the practice

In its letter dated 12.04.2005, the Federal Ministry of Finance commented on the input VAT allocation for credit institutions. It would first like to distinguish between different types of input supplies that credit institutions use for taxable and VAT exempt output supplies. For example, a turnover-based allocation key could be determined for IT services by means of machine runtimes. The Munich Tax Court rejected such a separation of IT services, at least with respect to the tax office’s estimate. This could help credit institutions to oppose such a separation, if necessary.

For other input supplies, the Ministry assumes that a "modified allocation key" should be applied and intends to base this modified key on the credit institutions’ margin – as is often the case with credit institutions. The result is to be modified again, e.g. by the number of credit transactions. This is, however, a mixture of two different calculation methods, which the Munich Tax Court considered not to be appropriate. The Federal Fiscal Court’s position on this remains open.

In other areas, the Federal Ministry of Finance wants to use (fictitious) flat-rate commissions or a service charge as a basis for calculation. This also raises the question of the admissibility of such a mixture. Against the background of these ambiguities and the Ministry’s statement in its letter of 12.04.2005 permitting other distribution methods, the Federal Fiscal Court decision allows for the conclusion that the so-called Philipowski method can no longer be applied without modification. However, each credit institution is still free to use an individual deductible proportion of input VAT.

Not only for credit institutions, but in general for the calculation of the deductible proportion of input VAT, the following applies: Each taxable person with partly taxable and partly VAT exempt output transactions may estimate its own deductible proportion. There are different calculation methods available for this purpose. Also different groups of input supplies can be formed to which different calculation methods are applied. The estimation only has to be appropriate which is a question of the individual case. In addition, it must be possible to substantiate the basis of estimation. Since this often requires documentation during the year (e.g. employee hours for certain projects), the taxable person should consider the appropriate (for him favourable) deductible proportion of input VAT in advance.