1 Background

The Residential Property Modernization Act (WEMoG) has recently turned the law on associations of residential property owners upside down. Thanks to sec. 9a of the Act on the Ownership of Apartments and Permanent Residential Right (WEG) new version, associations of residential property owners are becoming associations with full legal capacity. With this reorientation, the legislator is approaching to the general association law. The recent discussion on the status as taxable persons of communities of part owners (KMLZ Newsletter 09 I 2019) is thus a thing of the past for associations of residential property owners. Now, however, the ECJ has come up with a new issue. According to the current legal situation, associations of residential property owners provide non-taxable supplies, within the scope of their administrative tasks, which serve the overall interests of all members, and taxable special supplies to individual members (sec. 4.13.1. para. 2 sentence 1 of the German VAT Circular). Residential property owners are therefore facing a new VAT burden (unlike tenants or house owners). It was the original intention of the national legislator to prevent such a disadvantage for residential property owners (Bundestagsdrucksache IV/1590, p. 37 f.). In accordance with sec. 4 no. 13 of the German VAT Act, not only supplies by associations of residential property owners that affect the common property are exempt, but also supplies of heat and similar goods for the individual property of the property owners of the association.

2 New ECJ jurisprudence

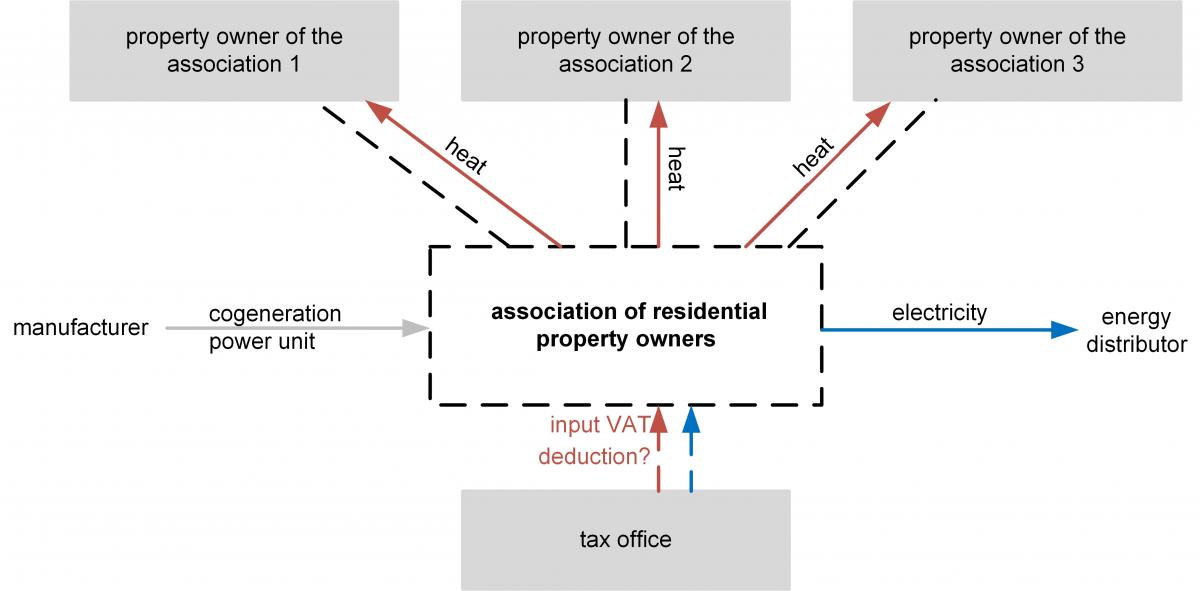

In its judgment of 17 December 2020 (C-449/19), the ECJ ruled that sec. 4 no. 13 of the German VAT Act is contrary to EU law. The underlying facts of the case were as follows: The Plaintiff, an association of residential property owners, built a cogeneration power unit on the property of its members. It supplied the electricity generated by this power unit to an energy distributor, while the heat produced was supplied to the property owners of the association. It then claimed input VAT deduction from the purchase and operation of the power unit. The tax office accepted a proportion of the input VAT deduction insofar as the input VAT burdened costs were attributable to the production of electricity. The tax office refused the input VAT deduction for the amount claimed relating to the production of heat. In this context, the Fiscal Court in Baden-Wuerttemberg referred the following question to the ECJ: Is the VAT exemption for the supply of heat by associations of residential property owners to the property owners of that association compatible with the EU VAT Directive?

This was clearly rejected by the ECJ. According to it, the EU VAT Directive does not provide for an exemption of heat supplies by associations of residential property owners to the property owners of that association. In the ECJ's view, the supply of heat to the property owners for their individual properties is deemed to be simply the sale of tangible property, which cannot be subject to the VAT exemption in accordance with Art. 135 para. 1 letter l of the EU VAT Directive, (“letting and easing of immovable property”), which is to be strictly interpreted.

3 Consequences for the practice

From a VAT perspective, the decision now leads to an unequal treatment of residential property owners as compared to tenants and house owners, something that the national legislator intended to prevent by means of sec. 4 no. 13 of the German VAT Act. If Germany wants to avoid infringement proceedings, the legislator will have to take action. Until then, associations of residential property owners (still) enjoy the protection of legitimate expectations pursuant to national law. An interpretation in conformity with the Directive contra legem would be inadmissible.

As for the rest, the decision opens up new possibilities: in future, associations of residential property owners can invoke the non-applicability of sec. 4 no. 13 of the German VAT Act and treat the supplies to their property owners as being taxable. This allows for subsequent input VAT deduction within the adjustment period in accordance with sec. 15a of the German VAT Act. Affected associations of residential property owners should therefore check whether the input VAT deduction eventually “pays off” in their individual case.

Moreover, the ECJ does not seem to have completely closed the door on VAT exemption. For the ECJ, it was decisive that in the case of a “supply” of heat, there was no longer any room for the assumption of a supply of rental services. In other words, it cannot be ruled out that other supplies of services by associations of residential property owners may fall within the scope of exempt supplies of rental services (Art. 135 of the VAT Directive). Charges for the use and maintenance of common property, the use of laundry rooms and washing machines, refuse collection or chimney cleaning could fall under the VAT exemption.

Contact:

Prof. Dr. Thomas Küffner

Lawyer, Certified Tax Consultant,

Certified public accountant

Phone: +49 89 217501230

thomas.kueffner@kmlz.de

As per: 14.01.2021