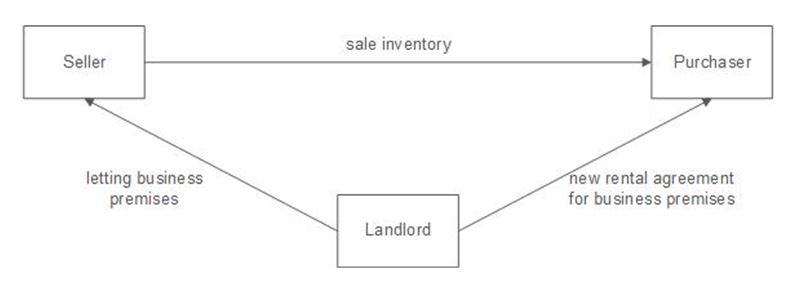

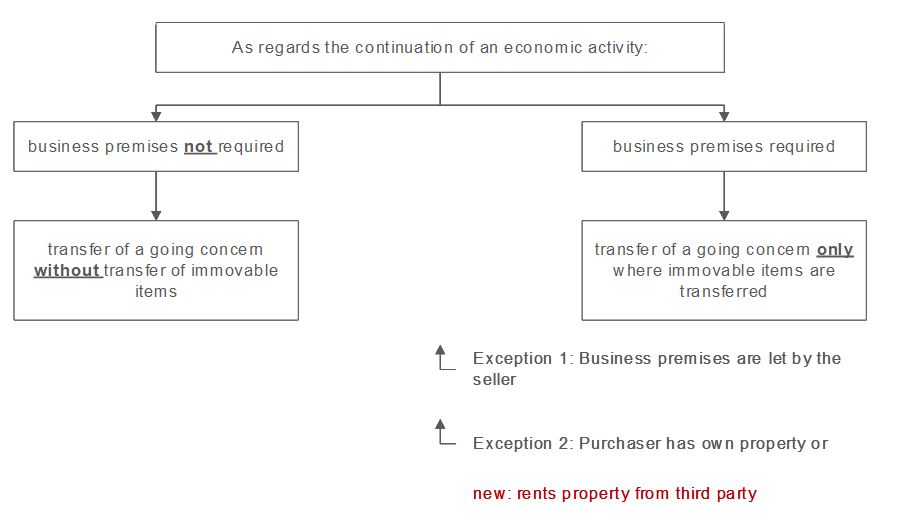

Thus, the question was whether or not it is harmful to the application of the TOGC principles that the business premises were not transferred and that, as a result, the purchaser was required to conclude his own rental agreement with a (third party) landlord. In other words, the case dealt with the following question: Is the transferred inventory a going concern?

In the Federal Fiscal Court’s opinion, this was the case. The national provision (sec 1 para a of the German VAT Act) is to be interpreted in conformity with Art. 19 of the EU VAT Directive. The decisive factor is whether the purchaser can continue the independent economic activity with the transferred assets. It is irrelevant that the purchaser concluded a separate rental agreement with a landlord. The Federal Fiscal Court refers to the important ECJ case law in the legal case Schriever. According to this, the question of whether the transferred going concern must include both movable and immovable property, is to be evaluated in view of the nature of the economic activity. In the disputed case, the business premises were inseparably linked to the inventory. Therefore, the immovable assets should also have been transferred. However, the Federal Fiscal Court makes an exception to this rule: It is sufficient if the business premises are made available to the purchaser, either by means of a rental agreement or if the purchaser himself owned a “suitable” alternate property. The latter – and this is new – can also be affirmed if the purchaser only has possession of the property on the basis of a separate rental agreement.

As regards the assumption that the business will be continued, in terms of the TOGC, the purchaser’s acquisition of individual items from third parties is irrelevant. It is, however, important that, from the acquirer’s perspective, the transferred items are sufficient for the continuation of the business. In practice, this results in the following testing scheme:

Contact:

Prof. Dr. Thomas Küffner

Lawyer, Certified tax consultant,

Certified public accountant

Phone: +49 89 217501230

thomas.kueffner@kmlz.de

As per: 07.11.2018