1 Background

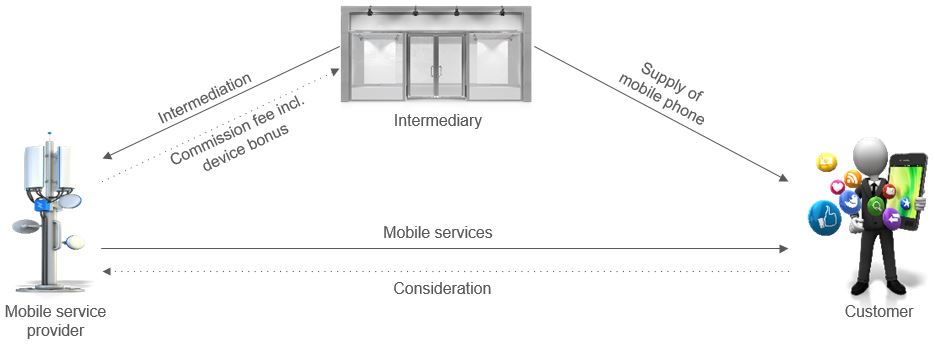

Intermediaries of mobile phone contracts are paid a commission by mobile service providers. In some cases, the commission also includes a so-called “device bonus”. This is usually related to the intermediary’s supply of a mobile phone to the customer.

In its judgment “Gratis-Handy (free mobile phone)” of 16 October 2013 “, the German Federal Fiscal Court (BFH) assumed that the device bonus, in the particular case, was to be treated as consideration paid by a third party (BFH, judgment of 16 October 2013 – XI R 39/12). The BFH affirmed a direct link between the supply of the mobile phones and the device bonus due to the contractual link between the device bonus and the supply of a mobile phone specified by the IMEI number. The Federal Ministry of Finance (BMF) adopted the BFH’s view (see sec. 10.2 para. 5 p. 7-8 of the German Administrative VAT Guidelines). In the opinion of the tax authorities, payment of consideration by a third party is given when the mobile service provider grants the intermediary a commission or a commission component, which is dependent on the supply of the mobile phone or other electronic item, on the basis of a contractual agreement. In the tax authorities’ view, these principles apply irrespective of whether the intermediary supplying the mobile phone for consideration or free of charge.

In practice, the question then arises as to how the so-called “indirect device bonus” should, from a VAT perspective, be treated. An indirect device bonus is deemed to exist if the said bonus is paid on the basis of a contractual agreement and the purpose of the agreement is to supply a mobile phone, but the intermediary is not contractually obliged to supply the mobile phone. In this case, the mobile service provider pays the device bonus to the intermediary, even though the intermediary may not have supplied a mobile phone to the customer.

2 BMF's letter dated 23 January 2024

In its letter dated 23 January 2024, the BMF once again comments on the VAT treatment of the device bonus. Clarifying the statements in sec. 10.2 para. 5 sentences 7-8 of the German Administrative VAT Guidelines, the BMF states that no consideration paid by a third party is deemed to exist when there is a contract between the mobile service provider and the intermediary, according to which the mobile service provider pays the intermediary a (final) commission, irrespective of the supply of a mobile phone to the customer (contractual decoupling). In this case, the commission, as a whole, constitutes consideration for the supply of intermediary services.

3 Consequences for the practice

The BMF rightly denies the payment of consideration from a third party in the case of contractual decoupling. This is because, in these cases, the direct link between the supply and consideration, which regularly arises from the legal relationship, ie the contractual relationship between the supplier and the recipient, is lacking. These principles also apply correspondingly to the assessment of whether a third party’s payment is granted for a specific supply rendered by the supplier. Accordingly, the indirect device bonus does not constitute consideration paid by a third party, as there is no contractual obligation on the part of the intermediary to supply a mobile phone.

In the event of a contractual decoupling, the device bonus is to be treated as consideration for the supply of intermediary services. The mobile service provider can deduct input VAT from the device bonus. The intermediary is not liable for VAT regarding the third party’s consideration. However, if the intermediary supplies a mobile phone, free of charge, this may constitute a supply carried out free of charge in accordance with sec. 3 para. 1b sentence 1 no. 3 of the German VAT Act. Mobile service providers and intermediaries should check their contracts to determine whether the device bonus is actually concisely decoupled from the supply of a mobile phone in their specific cases. This generally applies to donations in intermediary transactions, even beyond the mobile phone industry.

It remains incomprehensible why the BMF’s letter of 23 January 2024 only refers to the supply of mobile phones, even though in sec. 10.2 para. 5 sentence 7 of the German Administrative VAT Guidelines, the tax authorities refer to “the supply of the mobile phone or other electronic item”. The principles of the BMF’s letter of 23 January 2024 should also be applied to the supply of other electronic goods.