1 Background

In a letter dated 29 December 2025, the Federal Ministry of Finance published the templates for the VAT returns for 2026. In addition to changes for sales of military goods and the average rate for farmers and foresters, the new form contains a significant adjustment regarding the supplementary information for VAT returns (line 55, code number 500). In the templates from previous years, line 55 (code number 23) provided a free text field that could be used to submit various other information to the tax office.

2 Reform 2026

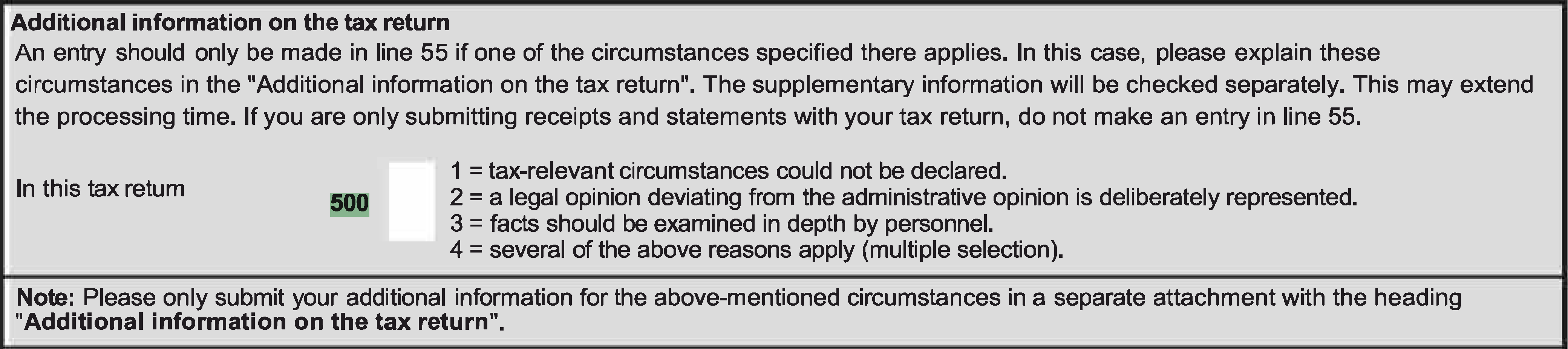

If additional information needs to be provided, the new code number 500 now requires classification into one of the four categories:

In addition, a detailed explanation in a separate appendix ‘Supplementary information on the VAT return’ will still be required.

3 Consequences for the practice

The Ministry does not comment on the specific reasons for the adjustment in the notes to the new templates and merely refers to changes of an ‘editorial nature’. Presumably, the categorisation of the supplementary information is due to the further development of risk management by the German tax authorities. The classification by the taxpayer allows the tax office to identify critical issues more quickly and deal with them in a targeted manner. If the taxpayer provides such supplementary information, this usually means that the VAT return is no longer subject to automatic VAT assessment and is processed manually. This can lead to delays and, in some cases, queries. There is also the possibility that an in-depth audit will call the entire VAT assessment into question. Such supplementary information should therefore be well prepared, especially if it deviates from the tax authorities' legal opinion. This includes, on the one hand, complete documentation of the facts and a thorough examination of the diverging legal opinions. If the supplementary information is used in a well-considered manner, it can also prove to be advantageous, for example by facilitating discussions concerning legally controversial issues with the tax office, from the outset. This can also help to avoid misunderstandings, e.g. in the context of a VAT audit. Furthermore, selecting number 3 may particularly be useful for coordinating the VAT classification of new circumstances with the tax office

4 Criminal tax law implications

It is also conceivable that supplementary information could have implications under criminal tax law. For example, allegations of tax evasion by omission can possibly be averted if it is communicated, at an early stage, that this is a deliberate deviation from the legal opinion of the tax authorities, or that the facts were still so unclear that they could not yet be conclusively clarified. It is crucial that no facts are concealed from the tax office and that the object of taxation and its basis of assessment are communicated so that the tax office can assess the VAT itself in case of doubt.

However, the new code number 500 also has an impact on the submission of voluntary disclosures and corrections. According to sec. 371 para. 2a of the German Fiscal Code (AO), it is possible to submit an effective partial voluntary disclosure for this VAT return period and the relevant facts by submitting a corrected VAT return. Unlike annual VAT returns, the requirement of completeness does not apply to the effectiveness of the voluntary disclosure. However, given that VAT is a mass tax, it must be checked whether the facts are also relevant for previous years. It is true that exemption from punishment is not excluded by sec. 371 para. 2 no. 2 AO if the discovery of the offence is based on the correction of a VAT return. However, it should be noted that for annual VAT returns, the requirement of completeness is a prerequisite for an effective voluntary disclosure. This means that the additional information provided regarding VAT must be complete for all assessment periods that are not time-barred. Therefore, similar or related circumstances must also be reviewed.

In the future, the new code 500 is also likely to blur the boundaries between voluntary disclosure under sec. 371 AO and notification and correction under sec. 153 AO, as the requirements of code 500 are likely to exceed the requirements for notification and correction under section 153 AO.

Businesses should take immediate action and adapt their process for submitting VAT returns to the new requirements. Employees involved in the process should be trained accordingly. In addition, entries in code 500 should only be made in accordance with the dual control principle and exclusively with the approval of the supervisor. Those making entries should be aware of the significance of their entries.

Contact