From 1 January 2027, the question of whether a legal entity under public law (jPdöR) is subject to VAT and has the status of a taxable person is governed solely by the regulations of sec.s 2 paragraph 1, 2b of the (German) VAT Act. In the course of the new taxation regime, the so-called ‘supply of assistance services’, which have been highly relevant in practice in the context of cooperation between public authorities and public bodies and which were previously irrelevant for VAT purposes under the old legal situation, will no longer apply.

In the future, all taxable supplies of a public authority – as with any other taxable person – will be subject to VAT under the general conditions of Sec. 2 paragraph 1 of the (German) VAT Act. In the future, an autonomous VAT assessment must therefore be carried out for each supply.

A supply of services by a legal entity under public law (jPdöR) is subject to VAT under the regime of Sec. 2b of the (German) VAT Act if the following questions can be answered with ‘YES’:

Was the supply rendered as part of a supply of goods and services for consideration?

Did the legal entity under public law act as a taxable person?

Was the supply taxable (i.e. not exempt from VAT)?

In the case of cooperation between jPdöR, all three conditions must be carefully considered!

Public bodies cooperation – a brief introduction

There are many different forms of cooperation between legal entities under public law and with a wide range of cooperation objectives. Examples include the many forms of cooperation in the context of municipal cooperation (e.g. in the areas of waste disposal, sewage disposal and water supply, fire brigades, health care, nature conservation, tourism, cultural and leisure facilities, etc.) or research and economic development cooperation.

The term ‘cooperation’ is not defined anywhere and it covers a wide range of different constellations. The simplest form of cooperation is a simple contract under the law of obligations in which one cooperation partner provides the other with a supply in return for reimbursement of expenses. However, cooperations can also take various forms under company law (e.g. the well-known ‘ARGE’). The form chosen in each individual case in turn has an impact on the value added tax treatment.

What are the VAT pitfalls for public-private partnerships between legal entities under public law?

Insofar as both cooperation partners are entitled to deduct input VAT, the cooperation is quite unproblematic from a VAT perspective. The recipient receives a refund of the VAT paid to the service provider as input VAT. The recipient is not charged VAT.

If, on the other hand, the recipient is not entitled to deduct input VAT, the VAT becomes a definite cost burden due to the lack of input VAT deduction! One of the reasons for this is that the recipient of the service uses the purchased supplies for non-taxable or tax-exempt output supplies. This means that the public sector, with its wide range of sovereign activities, is regularly unable to deduct input-VAT. In practice, the often unavoidable cooperation becomes a VAT problem.

Is there an exchange of supplies for consideration between the cooperation partners?

Usually, one cooperation partner provides compensation in the form of money for the activities of the other cooperation partner. This may be referred to in different ways (reimbursement of expenses, refund, compensation, etc.) or may be unspoken, depending on the individual case. In this case, the activity of the cooperating partner providing the service constitutes a taxable supply of services rendered in the context of an exchange of supply for consideration.

If the ‘compensation’ or ‘consideration’ is a payment in kind by the other, receiving cooperation partner, this is a so-called exchange-like supply. There is an exchange of supplies of goods and services. This is also subject to VAT.

The activities usually performed in the context of cooperation are therefore generally subject to VAT.

What solutions exist for avoiding a definitive VAT liability for the cooperation partners in the case of cooperation between legal entities under public law?

One approach to avoiding a VAT liability for the cooperation partners is based on the level of the supply of goods and services for consideration. This involves structuring the cooperation as a so-called expense pool in the form of an internal company.

1. Basics

In an expense pool, at least two individuals combine resources for the purpose of jointly procuring, developing or manufacturing assets, services or rights. The objective of the individuals involved is to derive mutual benefit from the combination of resources and skills. This may be based on cost savings, but also on non-economic reasoning, such as mutual recourse to specific know-how.

The group of participants in the expense pool is thus limited to persons who benefit from their supplies for themselves. They use their share of the results of the joint activity.

In personal terms, there are no restrictions. Thus, both legal entities under public law and third parties organised under private law can participate in an expense pool. The expense pool is therefore particularly suitable for cooperation with private individuals or non-profit organisations.

2. Definition of the expense pool

In an expense pool, each pool member performs tasks that are in the common interest of the pool. Each pool member has to make a previously agreed contribution. This often consists of the contribution or transfer of use of assets or the provision of other resources, such as the provision of own personnel capacities.

A key requirement for a ‘genuine’ expense pool is that no monetary compensation takes place! This also applies in the event that the cooperation partners make different contributions. A genuine expense pool therefore provides for general and complete gratuitousness. The contributions of the pool members are limited to the gratuitous cooperation.

If, on the other hand, compensation is paid in cash (so-called peak compensation), this compensation is subject to VAT according to the tax authorities (Sec. 1.6. para. 8 sentence 4 UStAE) (this is also referred to as a ‘non-genuine’ expense pool). Otherwise, the work shares are not subject to VAT in the amount of the agreed contribution obligation due to the fact that they are unpaid.

3. Summary classification and practical tip

Ultimately, the expense pool is comparable to an unincorporated internal partnership within the meaning of Sec. 705 of the German Civil Code (BGB). The internal partnership is distinguished from an external partnership (which is to be assessed independently in terms of VAT law) primarily by its non-participation in general legal and business transactions and the non-existence of joint assets.

Since there is currently no separate Federal Ministry of Finance's letter on expense pools from a VAT perspective, such a structure should always be secured by means of a binding ruling in accordance with Sec. 89 of the German Fiscal Code. At least the tax authorities seem to recognise the expense pool on the grounds of reasoning (see explicit differentiation from the expense pool in the Federal Ministry of Finance, Circular of 19 July 2022 - III C 3 - S 7189/20/10001 :001, BStBl. I 2022, 1208 on sec. 4 no. 29 (German) VAT Act).

When drafting the cooperation agreement – a draft of which is to be submitted with the application for a binding ruling – meticulous attention must be paid to compliance with the aforementioned requirements. Particular care is required in the clear and needs-based wording of the contributions to be provided by each of the cooperation partners. In particular, a clear distinction must be made between any further service relationships between the cooperation partners and, in individual cases, for consideration.

How is an expense pool structured in practice?

The following examples are intended to illustrate the practical implementation and the limits of the expense pool in practice.

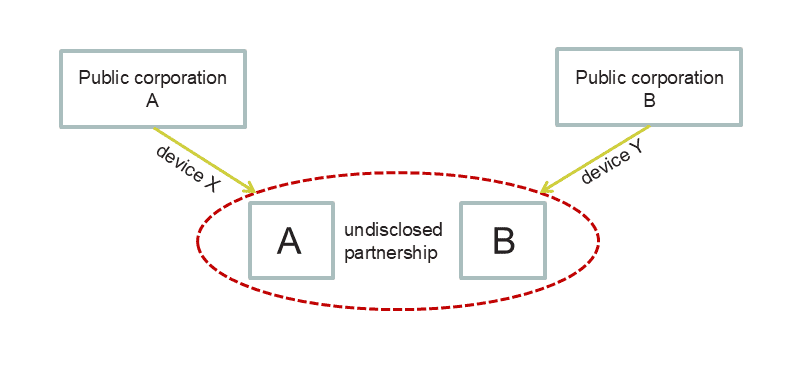

Example: A and B, both public corporations, agree in the context of a cooperation contract that they want to cooperate in the operation of a building yard. Since the provision of all equipment and machinery would exceed the financial means of the individual public corporations, they agree that A will provide the other with device X and B will provide the other with device Y, each to a certain extent.

VAT classification: The mutual transfer of the equipment and consumables (respective shares of work) does not result in supplies of goods and services for consideration due to the lack of consideration. No VAT relevance.

Variation on the initial case: Since operating equipment X is significantly more expensive than operating equipment Y, B covers part of the operating costs and makes a refund to A.

VAT classification: The mutual provision of equipment (respective share of work) does not constitute supplies of goods and services for consideration due to the lack of consideration. Insofar as there is no VAT relevance.

By contrast, the additional reimbursement of costs from B to A represents a deductible and taxable peak compensation. In such cases, one also speaks of a so-called ‘pseudo expense pool’.

What other options are there for avoiding a definitive VAT charge on the cooperation partners, taking into account Sec. 2b of the (German) VAT Act?

Further potential solutions for avoiding a definitive VAT burden on the cooperation partners arise at the level of the taxable person in the case of public authorities. It follows from Sec. 1 para. 1 no. 1 sentence 1 of the (German) VAT Act that only the supplies of a taxable person are subject to VAT.

If the services are not provided free of charge in exceptional cases (e.g. in the case of a genuine expense pool, see above) the status of the public body as a taxable person under Sec. 2 para.1 of the (German) VAT Act is generally to be affirmed in the context of cooperative collaboration. The ‘general concept of a taxable person’ (Sec. 2 para. 1) (German) VAT Act) will be defined in more detail for legal entitles under public law from 1 January 2027 by Sec. 2b (German) VAT Act.

If the scope of Sec. 2b of the (German) VAT Act applies in an individual case, the taxable status of the cooperation partners may be restricted in individual cases via Sec. 2b of the (German) VAT Act. According to Sec. 2b para. 1 of the (German) VAT Act, legal entities under public law are not considered taxable persons if they act in the exercise of official authority and no significant distortions of competition (general reservation of competition) are threatened.

1. Scope of application of Sec. 2b of the (German) VAT Act

The legal entity under public law can only invoke the exceptions of Sec. 2b of the (German) VAT Act if Sec. 2b of the (German) VAT Act is applicable at all. Therefore, the activity carried out by the legal entity under public law in the individual case must be ‘in the exercise of official authority’ (known as the reservation of sovereign rights).

The only activities that can be considered to be the responsibility of a legal entity under public law in the exercise of official authority are those in which the legal entity under public law acts on the basis of a special regulation under public law (see Federal Ministry of Finance, Circular of 16 December 2016 - III C 2 - S 7107/16/10001, BStBl. I 2016, 1451, para. 6 et seq.). A special regulation under public law may arise in particular from a law or public-law contracts (see Federal Ministry of Finance, Circular of 16 December 2016, para. 12 et seq.).

If, on the other hand, a legal entity under public law acts under private law, these activities are generally not covered by sec. 2b of the (German) VAT Act. Acting under private law generally precludes the applicability of sec. 2b of the (German) VAT Act!

If there is no (rarely encountered) legal cooperation (see 3.) and the cooperation partners want to open up the scope of § sec. 2b of the (German) VAT Act, the cooperation should be regulated in a public-law contract insofar as possible.

Of course, a public-law contract with private individuals will almost invariably be ruled out. Therefore, (German) VAT Act §2b is only of practical significance for co-operations between legal entities under public law. Nevertheless, individual supplies to private individuals may not be taxable under the conditions of (German) VAT Act §2b (e.g. supplies that are provided only occasionally and to a small extent, cf. sec. 2b, para. 1 no. 1 of the (German VAT Act).

2. No (effective) way out via sec. 2b para. 3 no. 2 of the German VAT Act (UStG)?

KMLZ VAT NEwsletter 45/2019: Public Bodies: Gradual Extinction of Cooperations – "Started out a tiger, but ended up a bedside rug")

Since the term ‘significant distortions of competition’ remains a mystery, the legislator included four examples in sec. 2b para. 3 no. 2 of the German VAT Act (UStG), in which distortions of competition are excluded from the outset and the legal entities under public law are to be non-taxable persons. The regulation was intended to favour, under VAT law, cooperation between legal entities under public law and thus ultimately to ‘save’ the assistance services that were not taxable under the old law.

However, the VAT Directive does not provide for or create any such VAT advantages for cooperation between legal entities under public law. The European Commission therefore had doubts as to whether the German regulation was in conformity with EU law. In order to avoid infringement proceedings, the German tax authorities responded with the Federal Ministry of Finance decree, Circular of 14 November 2019 – III C 2 – p. 7107/19/10.005:011, BStBl. I 2019, 1140.

According to the Circular, even if the cumulative conditions of sec. 2b para. 3 no. 2 of the German VAT Act (UStG) are met, a separate examination of possible significant distortions of competition within the meaning of section 2b para. 1 sentence 2 of the German VAT Act (UStG) (general proviso regarding competition) is mandatorily to be carried out.

In view of the Federal Ministry of Finance's letter, sec. 2b para. 3 no. 2 of the (German) VAT Act now merely represents a standard example, the presence of which does not obviate the need for a separate examination of the general proviso regarding competition. This means that in practice the regulation is virtually ineffective.

3. Solution via sec. 2b para. 3 no. 1 of the (German) VAT Act?

The wording already indicates that the exemption under sec. 2b para. 3 no. 1 of the (German) VAT Act only applies to the cooperation of legal entities under public law in the fulfilment of public tasks (see Federal Ministry of Finance, Circular of 16 December 2016, para. 40). Thus, only cases of administrative assistance or the so-called assistance and cooperation services between legal entities under public law are covered. The regulation generally does not apply to cooperation with private individuals!

According to § 2b, para. 3, no. 1, competition and thus significant distortions of competition are excluded:

for supplies that are legally reserved for legal entities under public law or whose provision is legally denied to private economic operators

as well asfor supplies that a legal entity under public law may only request from another legal entity under public law due to applicable legal provisions.

In deviation from the ‘special regulations under public law’ within the meaning of Section 2b para.1 of the (German) VAT Act (see under 1.), all laws and ordinances of federal or state law as well as the special legislation of the churches are to be understood as statutory provisions within the meaning of Section 2b para. 3 no. 1 of the (German) VAT Act. According to the legal provisions, only a legal entity under public law may act as the supplier and thus the provider of the service. There must be a ‘statutory monopoly’ in favour of a legal entity under public law.

The legal basis must be formulated in such a way that the supplies specifically required by the other legal entity under public law may only be provided by another legal entity under public law (see Section 2b.1 para. 8 UStAE). The legal regulation of a merely general requirement to cooperate is insufficient. It is not possible to fill in or substantiate this requirement by means of sub-statutory regulations, contractual agreements or actual administrative practice.

The problem with this solution is that the cooperation partners have no say in the matter. The cooperation partners will regularly be dependent on the federal or state legislator to create a precise legal monopoly.

However, the provisions of state law that have been enacted recently (in some cases as evidenced by the official justification for the law) to implement Section 2b para. 3 no. 1 of the German VAT Act (draft) show that actively approaching the legislator and explaining the impending VAT consequences can be quite effective! After all, it is not uncommon for the state budget to be at stake.

Regardless of Section 2b of the (German) VAT Act, what options are there regarding the status as taxable person to avoid a VAT charge for the cooperation partners?

In the case of cooperation between parent and subsidiary companies, the grounds for a VAT group in accordance with sec. 2 para. 2 no. 2 of the (German) VAT Act are still conceivable.

In the case of a VAT group, only the ‘controlling company’ – and not the ‘VAT group’ as such – is a taxable person (according to the German understanding). The controlled company is a dependent part of the controlling company's business. Consequently, supplies within the VAT group are already not subject to VAT (so-called internal supplies) (according to the prevailing understanding to date).

The VAT group thus has economic advantages if the input VAT deduction of a controlled company/the controlling company is (partially) excluded, for example, in the case of activities of legal entities under public law in the non-economic sector.

The VAT group is formed by operation of law when all the legal requirements are met and ends when one of the legal requirements no longer applies. There is no right to choose or apply.

The legal requirements include the so-called financial, organisational and economic integration. The respective requirements are set out in detail by the tax authorities in sec. 2.8 of the VAT Application Decree. In the case of cooperation between a legal entity under public law and its subsidiary (e.g. in the municipal sector), the requirements for a VAT group can often be met with minor organisational measures.

Unfortunately, there is currently no legal certainty for legal entities under public law regarding VAT groups.

According to German legal understanding, both the controlling company and the controlled company must fulfil the criteria for being a taxable person under VAT law. Consequently, non-taxable persons – i.e. legal entities under public law that act exclusively in a sovereign or non-commercial capacity – generally cannot be part of a VAT group. The ECJ has expressly ruled that non-taxable persons can also be ‘members’ of a VAT group (KMLZ VAT Newsletter 50/2022: Potential for structuring: VAT group also includes non-economic activities). Conversely, this means that legal entities under public law can only be controlling companies under German law if and insofar as they are economically active.

It is encouraging, however, that the ECJ – after repeated submissions by the German Federal Fiscal Court (decision of 26 January 2023 – V R 20/22 (V R 40/19), BStBl. II 2023, 530) – recently clarified that internal transactions are not subject to VAT, regardless of the VAT group recipient's entitlement to deduct input VAT (ECJ, judgment of 11 July 2024 – C-184/23, S/FA T II). The ECJ thus expressly and unreservedly confirmed the previous and current legal interpretation of the Commission, the German Federal Fiscal Court and also the German tax authorities. In this respect, there can be collective relief. The discussion regarding the taxability of internal transactions within the VAT group, which has flared up in the meantime, should now have come to a conciliatory conclusion.

Nevertheless, in view of the continued lack of legal certainty, the specific grounds for a VAT group should be well prepared and agreed with the tax authorities in the form of a binding ruling.

Which VAT exemptions can practically avoid a VAT burden on the cooperation partners in the case of cooperation between legal entities under public law?

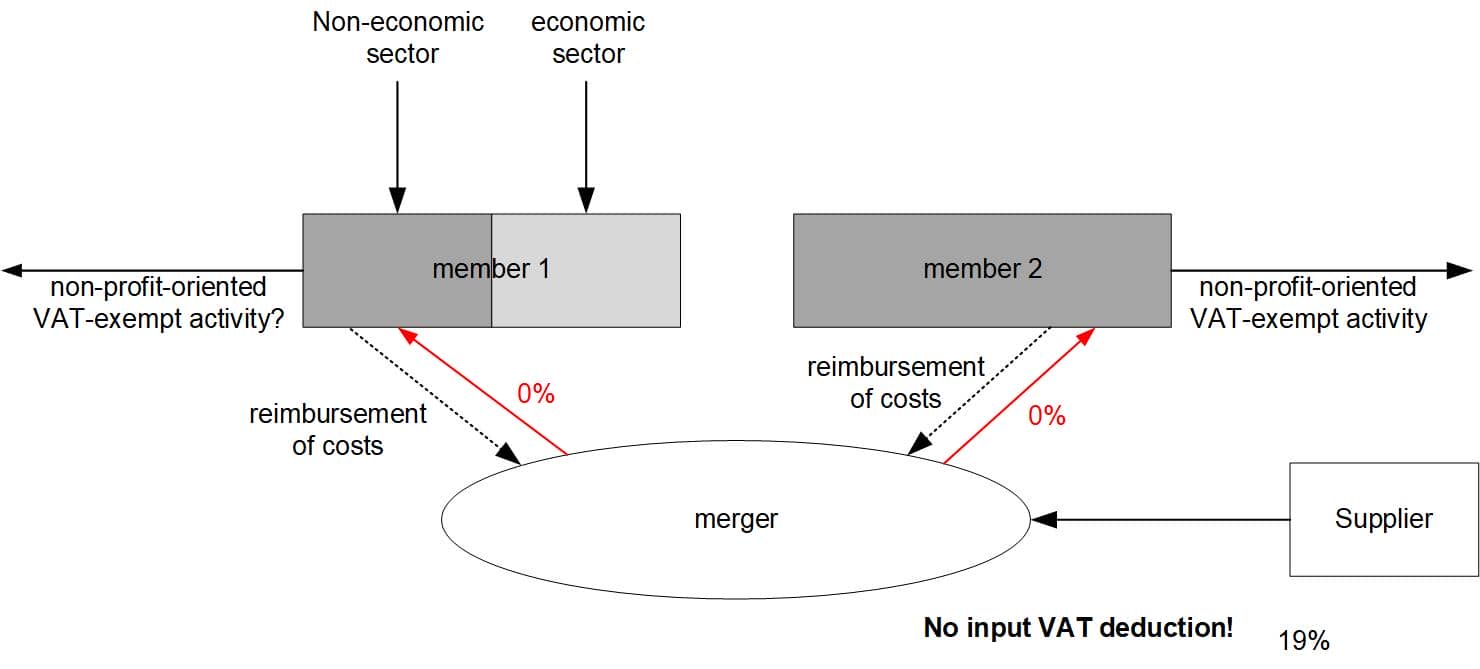

The VAT exemption under Section 4 No. 29 of the German VAT Act offers legal entities under public law and non-profit organisations the opportunity to cooperate with each other without incurring VAT.

The cost pool is distinguished from the cost community by the fact that it goes beyond a mere cost sharing agreement. The wording of the regulation itself presupposes an independent association of persons. Furthermore, there can only be talk of an association when at least two individuals – the members – come together and appear as such to the outside world (external company).

The following are associations within the meaning of section 4 no. 29 of the (German) VAT Act: partnerships and corporations, registered cooperative societies, registered associations, property ownership communities, special-purpose associations, public-law institutions and other legal entities under public law. The legal form and legal capacity of the association or its participating members are not relevant.

According to Section 4 No. 29 of the (German) VAT Act, the provision of services by independent associations of individuals to their members is VAT exempt if the following cumulative conditions are met:

The members must use the supplied services directly in the pursuit of activities that serve the public good. This applies to activities that are already not subject to VAT or are VAT exempt under Section 4 Nos. 11b, 14 to 18, 20 to 25 or 27 of the (German) VAT Act.

The agreed and actually paid consideration may only consist of the exact reimbursement of costs. All costs that the association incurs in the interest of its members, in particular personnel and material costs, may be passed on.

Finally, the exemption must not cause any distortion of competition. The concept of competition in sec. 4 no. 29 German VAT Act is to be interpreted autonomously and must not be equated with the competition proviso in sec. 2b German VAT Act (see above). For sec. 4 no. 29 German VAT Act, the decisive factor is whether the exemption itself can directly lead to distortions of competition. There is no risk of distortion of competition if the association is or can be sure that its members will remain customers regardless of whether they are subject to VAT or exempt from it. This is likely to be the case as a general rule, since only an unselfish association will be satisfied with the exact reimbursement of costs. A private third party would not be willing to forgo a mark-up to generate a profit.

If the requirements of Section 4 no. 29 of the (German) VAT Act are met, the association may provide its supplies to its members on a VAT-exempt basis:

However, this does not apply the other way around. It is therefore a ‘one-way street’. Supplies to third parties are also not VAT exempt.

Fortunately, the Federal Ministry of Finance has provided some legal clarity in the context of Section 4 no. 29 of the German VAT Act in its letter dated 19 July 2022 (Federal Ministry of Finance, letter dated 19 July 2022 – III C 3 – S 7189/20/10001 :001, Federal Tax Gazette. I 2022, 1208) provided a little legal clarity in the context of section 4 no. 29 of the (German) VAT Act. In detail, however, the vague legal concepts of immediacy, cost recovery and exclusion of competition continue to cause problems and interpretation difficulties in practice.

The specific structure of the cost pool should therefore always be verified with the relevant tax office by obtaining binding information. In any case, with the issuance of the Federal Ministry of Finance's letter dated 19 July 2022, there should no longer be any doubts on the part of the tax authorities regarding the admissibility of such binding information. A case of AEAO on Section 89 no. 3.5.4. does not exist if the taxable person's sole intention is to substantiate the vague legal terms used by the legislator and the Federal Ministry of Finance in an individual case.

Contact