For VAT purposes, every legal entity under civil law is, in principle, an independent taxable person. This applies at least if the entity independently carries out a business or professional activity (see sec. 2 para. 1 sentence 1 of the German VAT Act (UStG)). By way of derogation, VAT groups mean that two persons who are (still) independent under civil law become one taxable person for VAT purposes (VAT group).

The VAT group is governed by sec. 2 para.2 sentence 2 of the German VAT Act. Its basis in Union law is Article 11 of the VAT Directive.

Such a VAT group has legal consequences in various sectors. The following questions illustrate this diversity:

Who files VAT returns?

How are supplies between group members (so-called internal supplies) treated?

Does the non-taxable sector of a group member also form part of the VAT group?

What are the implications for input VAT deduction?

Which group member must be stated on incoming and outgoing invoices?

What happens if the VAT group is identified too late or if it ceases to exist without being noticed?

Before considering these consequences, the key question is whether the requirements for a VAT group are met in the first place.

What are the requirements for establishing a VAT group?

There are essentially five requirements for a VAT group. First, both the controlling company (Organträger) and the controlled company (Organgesellschaft) must each qualify as taxable persons for VAT purposes. In addition, the three integration criteria—financial, economic, and organisational integration—must be fulfilled. Unlike in the case of income tax groups, a profit and loss transfer agreement is not required.

1. Controlling company and controlled company as taxable persons

Both the controlling and controlled companies must be taxable persons for VAT purposes, in order to be part of a VAT group. The German Federal Fiscal Court (BFH) has reaffirmed this, even though it is not strictly required under Union law.

In particular, the status of controlled companies, as taxable persons, must be carefully examined within groups. Gaining this status is often problematic for legal entities under public law. Finally – although this issue rarely arises in practice – the status as a taxable person of non-profit organisations must be examined on a case-by-case basis with regard to their non-economic sector.

2. Financial integration

Financial integration means that the controlling company must hold the decisive majority of voting rights. It must be able to impose its will in the shareholders’ meeting of the subsidiary (see KMLZ Newsletter 17/2023 for financial integration with only 50% of voting rights). Financial integration can also be achieved through a chain across several companies (parent – subsidiary – sub-subsidiary).

As a rule, the parent company must hold more than 50% of the shares in the subsidiary. Only in exceptional cases can a smaller share of the company shares be sufficient (eg in the case of multiple voting rights or a voting rights agreement in accordance with the articles of association). In other cases, a higher shareholding is required. This applies, for example, if the articles of association provide for qualified majorities for a large number of decisions.

According to the German Federal Fiscal Court (BFH) and the tax authorities, however, sister companies cannot form a VAT group on their own without the involvement of the common shareholder (see KMLZ Newsletter 36/ 2022: No VAT group between sister companies).

3. Organisational integration

Organisational integration requires that the controlling company can impose its will on the day-to-day management of the controlled company. It is not sufficient for the controlling company to be able to issue instructions to the management of the controlled company via the shareholders’ meeting.

Organisational integration is assessed on the basis of a tiered system. The best way to achieve integration is for all managing directors of the subsidiary to also be managing directors or board members (ie decision-making bodies) of the parent company (tier 1).

Under certain conditions, organisational integration can also be established by employees of the parent company, depending on the legal form of the subsidiary. However, organisational integration cannot be justified on the grounds that the managing directors of the parent company are merely authorised signatories or similar of the subsidiary.

If some managing directors/board members of the subsidiary are also part of the decision-making body of the parent company, organisational integration is possible (second tier), provided these identical persons can impose their will in all management decisions of the subsidiary. This often requires the subsidiary’s managing director regulations, for example, to be structured accordingly.

When these persons are not identical, there is generally no organisational integration (third tier). In such cases, significant structuring is required to establish organisational integration, which is only possible if the controlling company has institutionally secured direct intervention rights in the core area of day-to-day management. In most cases, legal uncertainties remain, so that such grounds for a controlling relationship are primarily used in “defensive advice”. Alternatively, organisational integration can be achieved by means of a control agreement, which is a legally secure option.

4. Economic integration

In practice, it is often difficult to determine economic integration in a legally secure manner. Unlike financial and (partly) organisational integration, it cannot be determined mathematically. Instead, the parent and subsidiary must be closely economically interlinked.

This can usually be achieved through supplies provided by the parent company to the subsidiary, for consideration. However, supplies provided by a controlled company to a sister company for consideration can also serve as grounds for the indirect economic integration of the sister company (see KMLZ VAT Newsletter 40/2023: VAT group: indirect economic integration). However, these supplies provided for consideration must be of more than insignificant importance. For example, supplies of bookkeeping services and winter road maintenance services provided for consideration are not sufficient to establish the necessary level of economic integration. In this respect, each case must be considered on a case-by-case basis.

A recent judgment by the German Federal Fiscal Court (BFH, judgment of 1 February 2022 – V R 23/21), which the German Federal Ministry of Finance has also incorporated into the German Administrative VAT Guidelines (UStAE), has increased uncertainty on economic integration, particularly in the sector of frequent rentals. The courts seem to interpret this criterion quite restrictively (see KMLZ VAT Newsletter 36/2022: No VAT group between sister companies).

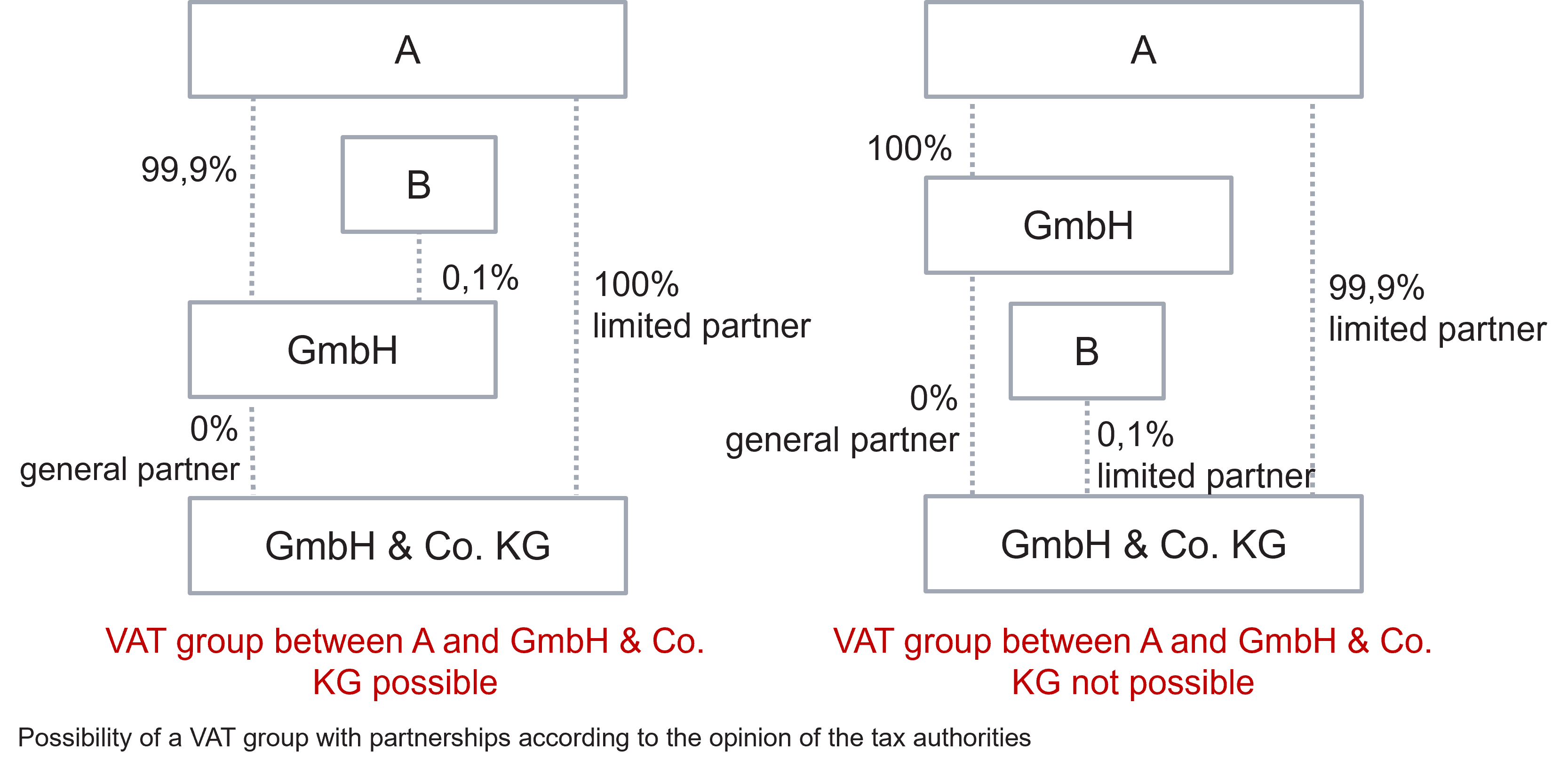

5. Partnerships as controlled companies

In recent years, there has been considerable controversy as to whether a partnership can also be a controlled company. The reason for this dispute is that, according to the wording of the German VAT Act, only ‘legal entities’ can be controlled companies.

Meanwhile, the two German Federal Fiscal Court senates responsible for VAT have agreed that at least a GmbH & Co. KG can be a controlled company under the same conditions as any other company. It remains unclear what the situation is for other types of partnerships (KGs, OHGs, GbRs), as there is, as yet, no German Federal Fiscal Court decision on this issue.

According to the (still) current opinion of the tax authorities, all partnerships can be controlled companies if, in addition to the controlling company, they only have shareholders who are financially integrated into the controlling company. In the opinion of the tax authorities, the first step is therefore to determine who the shareholders of the partnership are. The second step is to check whether these shareholders are either the controlling company itself or whether they are financially integrated into the controlling company.

However, there are already instructions from some state tax authorities to the effect that, under certain conditions, VAT groups can rely on the more extensive German Federal Fiscal Court jurisprudence.

What are the legal consequences of a VAT group?

If the requirements for a VAT group are met, this has legal consequences in a wide variety of sectors.

1. Internal supplies are non-taxable

According to the wording of sec. 2 para. 2 no. 2 of the German VAT Act, the main legal consequence of a VAT group is that the controlled company becomes a dependent part of the controlling company. Instead of two companies, there is only one company.

As a result, civil law supplies between the members of a group of companies are non-taxable. The German Federal Fiscal Court recently confirmed this lack of taxability of internal supplies (see KMLZ Newsletter 31/2024: The ECJ has ruled: Internal supplies within a VAT-Group are not subject to VAT and 56/2024: VAT Group: New tax model for legal entities under public law and non-profit organisations). This also results in the essential effect of the VAT group. This lack of taxability of internal supplies results in economic advantages insofar as the parties involved in the group are not entitled to deduct full input VAT (e.g. banks, insurance companies, hospitals and other taxable persons operating in the social sector).

2. Practical consequences of the VAT group

In practice, the assumption of a business entity consisting of a controlling company and a controlled company means that the controlled company itself no longer has to file VAT returns. Instead, the controlling company also declares, in its VAT return, the supplies carried out by the controlled company under civil law. Accordingly, the controlling company claims input VAT deduction for supplies purchased from the controlled company under civil law.

Despite this, the controlled company may issue outgoing invoices in its own name (and using its own VAT-ID). For incoming invoices, it is also sufficient for the controlled company to be named as the recipient. This means that the VAT group does not have to be disclosed to third parties.

If the controlled company carries-out intra-Community supplies, it must declare these in its own EC Sales List. If the controlling company declares the intra-Community supplies carried out by the controlled company under civil law in its EC Sales List, these are taxable in accordance with sec. 4 no. 1 lit. b half sentence. However, this can usually be corrected retrospectively.

3. Scope of the VAT group

Various taxable persons, such as legal entities under public law or holding companies, may have a taxable and a non-taxable sector. The German Federal Fiscal Court recently confirmed that the non-taxable sector (eg the sovereign area) of a controlling company is also included in the VAT group (see KMLZ Newsletter 56/2024: VAT Group: New tax model for legal entities under public law and non-profit organisations). In the following diagram, the red circle (and not the blue one) therefore symbolises the group of companies. This means that supplies provided by the controlled company, in the non-taxable sector of the controlling company, are also not subject to VAT as internal supplies. However, the German Federal Fiscal Court left open the question as to whether this also applies in the opposite direction, ie to supplies provided by a controlling company that is exclusively active in the taxable sector, to the non-taxable sector of a controlled company

The tax authorities currently take a different view (namely that the supplies of services shown in red are taxable. However, they would use different grounds. They assume that the non-taxable sector of the controlling company is not part of the VAT group. In the above diagram, the blue circle would form the group of companies in the opinion of the tax authorities. Since the supplies of services marked in red “leave” this group of companies, they are taxable according to the tax authorities. By referring to the jurisprudence of the German Federal Fiscal Court, tax advantages may therefore arise, particularly in the public sector and for non-profit organisations, but also for mixed holding companies.

4. Input VAT deduction

When deducting input VAT, the first step is to directly allocate procured goods and services to the output transaction. If such a direct allocation is successful, the VAT group has no effect on this. The input VAT deduction is determined by the type of output transaction.

However, with regard to general expenses, the VAT group does have an effect on input VAT deduction. This applies in cases where one of the companies involved in the group also has output transactions that do not qualify for input VAT deduction (eg certain VAT exempt output transactions). In these cases, the existence of a corporate entity means that the output transactions of the controlled company also affect the input VAT ratio of the controlling company and vice versa.

In this respect, it must be decided in each individual case, whether an input VAT ratio is to be determined for the entire company or whether different input VAT ratios apply to different types of procured goods and services. This gives the taxable person some leeway in the context of the appropriate estimate to be made (sec. 15 para. 4 sentence 2 of the German VAT Act).

5. Unrecognised existing or ceased VAT group

The VAT group for VAT purposes arises when the relevant conditions are met. No application, approval, notification to the tax office or similar is required. This can lead to surprises, for example, in the context of a tax audit, in the event of insolvency or during a review by the taxable person themselves or their tax consultant.

It is possible that the requirements for a VAT group are not met despite the parties acting as if they were (unrecognised ceased VAT group), or that the requirements are met without the parties being aware of this fact (unrecognised existing VAT group).

Unrecognised existing VAT groups usually have less impact. The controlled company will have declared its own VAT and will be refunded the tax paid plus interest. The controlling company must pay VAT in the same amount plus interest. These amounts often offset each other.

Even if VAT is shown on invoices for supplies between the controlling company and the controlled company, no VAT arises in this respect in accordance with sec. 14c of the German VAT Act. These are only internal accounting documents and not invoices in terms of VAT law. Nevertheless, it must be carefully checked, in each individual case, whether the above statements also apply in this respect. Deviations from this are certainly conceivable.

Unrecognised ceased VAT groups have more significant consequences. Internal supplies must be taxed retroactively, and interest is often due. Since VAT was not previously shown on invoices between group members, there is no retroactive input VAT deduction, and the new input VAT amounts are not interest-bearing in favour of the business.

In such cases, the legal consequences must generally be examined comprehensively and the VAT implications for all parties involved in the group of companies must be calculated. This usually involves considerable effort, which can significantly outweigh the tax loss. It is possible to attempt to avoid a “reversal” by means of entering into dialogue with the tax authorities. However, the precise nature of communication with the tax authorities must be carefully considered in such cases.