1 Background

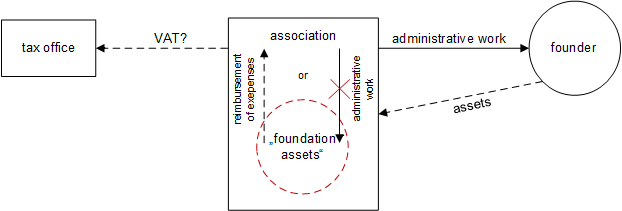

In its judgment of 5 December 2024 (V R 13/22), the German Federal Fiscal Court (BFH) ruled that the administration of dependent foundations, in return for reimbursement of expenses from the foundation’s assets, (the question being whether this constitutes “consideration”), may represent a VAT-relevant supply to the founder (see KMLZ VAT Newsletter 15 | 2025). According to the BFH, a taxable supply to the founder may also exist in relation to assets that are, under civil law, owned by the administrator (or trustee - in the BFH case, an association). The prerequisites are that the assets (1) are subject to special restrictions as special assets, (2) are kept separate from the administrator’s other assets, and (3) the administrator receives consideration for their services. In the BFH’s view, the founder receives a consumable benefit, as the asset management is carried out in the founder’s interest. This applies at least during the founder’s lifetime. However, a supply by the administrator to the special assets themselves is not possible.

The BFH’s judgment is unconvincing and has rightly been subjected to considerable criticism: the founder does not, in fact, receive a consumable benefit. Rather, the founder transfers assets, subject to a condition. The only beneficiary is the charitable purpose itself, which, due to insufficient legal independence, cannot be regarded as a proper recipient of a supply for VAT purposes. This is also evident from the donation certificate under sec. 10b of the German Income Tax Act, which the founder receives for the full amount of the donation. The inconsistency of the BFH’s legal consequences is further demonstrated by the fact that, upon the founder’s death, the BFH sees the end of VAT liability, as there would no longer be an identifiable recipient of the supply.

2 BMF letter of 8 December 2025

Alarmingly, the tax authorities – presumably for fiscal reasons – are following the BFH’s lead. The Federal Ministry of Finance (BMF) intends to assume a supply for consideration: The administration of fiduciary foundations by a trustee may constitute a taxable supply of services for consideration which is subject to VAT if a reciprocal contract exists with the founder and the assets are managed as special assets. Thus, in addition to the separate management of the assets, a reciprocal contract with the founder must also exist. The BFH affirmed such a contract as, in the case at hand, an agency agreement for services for consideration had been concluded between the trustee and the trustor. In this context, the BFH repeatedly emphasized that both parties could terminate this contract at any time. This may offer a practical approach: “less is more” – the fewer provisions the parties agree upon, the better for VAT purposes.

It is highly problematic that the BMF does not provide for any transitional arrangements for trustees. The new view is therefore to be applied to all open cases. Trustees must now review all trust agreements to determine whether consideration has been received and, if so, whether a VAT-relevant legal relationship exists that also involves separate asset management.

Interestingly, the BMF is planning a transitional arrangement for cases in which dependent foundations have previously been treated as independent suppliers. In practice, this occurs when dependent foundations, for example, provide taxable administrative or rental services to third parties. Such supplies must be treated as supplies of the trustee as of 1 January 2027 at the latest.

3 Reference for the Practice

The bottom line: No good deed goes unpunished. The tax authorities want their share here as well. They could have assessed the situation differently – and with good reason. It is disconcerting that trustees must now “clear up” their past. They often act in pursuit of charitable objectives and previously believed themselves to be on safe ground for VAT purposes. That is no longer the case. The political leadership of the BMF must consider whether such charitable foundations should, in future, only be established upon death, (when there is no VAT-relevant recipient of the supply), or whether it is better for trustees to generally waive reimbursement of expenses. Neither approach serves the common good. Fiduciary foundations make a significant contribution towards relieving the public purse. The tax authorities need not worry, as the donated assets are bound for charitable purposes. The BMF would do well to promptly revise its circular. A model wording from the BMF on when a VAT-relevant legal relationship is to be denied would provide much-needed legal certainty. Despite all the frustration: the BMF has clearly stated that a supply for consideration may occur. This means there are also ways out. In such cases, however, the consequences of a possible supply of services carried out free of charge must also be considered.

Contact