1 Background

The intra-Community triangular transaction in sec. 25b of the German VAT Act (Art. 42, 141 and 197 EU VAT Directive) is a simplification rule for certain chain transactions. In such a transaction, the purchaser of the supply the transport is ascribed to is generally required to register for VAT purposes in the country of destination. If the purchaser uses a VAT-ID that does not originate from either the dispatch or destination Member State, this registration requirement can be avoided. The VAT liability for the subsequent supply in the destination country is transferred to the customer, and the intra-Community acquisition is deemed to have been taxed there.

So far, so simple. In practice, however, the application is restrictive. Member States interpret the conditions differently. Divergences exist, particularly regarding existing registrations, the number and position of parties in the chain, and EU establishment. These differences create significant risks for taxable persons seeking to benefit from the triangular transaction simplification. If the simplification is denied, acquisition taxation under sec. 3d sentence 2 of the German VAT Act (Art. 41 EU VAT Directive) applies in the Member State of the VAT-ID used.

2 Facts of the case

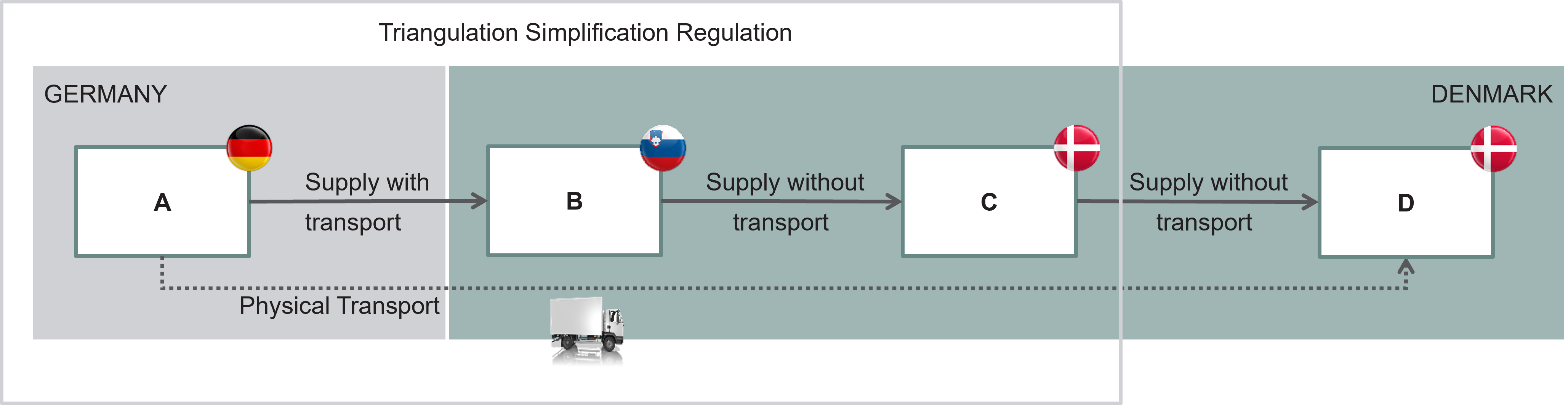

The case referred to the General Court dealt with a chain transactions involving more than three parties. The supply chain involved four taxable persons rather than the “classic” triangular transaction with three parties. One taxable person with a German VAT-ID (A) supplied goods to a taxable person with a Slovenian VAT-ID (B). B supplied the goods to a taxable person with a Danish VAT-ID (C). C then supplied them to another taxable person, also with a Danish VAT-ID (D). The transport of the goods was carried out directly from Germany to Denmark and was organised and paid for by B.

The question was whether C was required to physically take possession of the goods. The court also examined whether the simplification could apply if B was involved in tax fraud, as C was a missing trader.

3 Judgement

The General Court concluded in its decision of 3 December 2025 (T-646/24) that the triangular transaction simplification can apply to chain transactions involving more than three parties, provided the conditions of Art. 141 EU VAT Directive are met. It is not detrimental if the final purchaser in the triangular transaction is not the last purchaser in the chain transaction. The decisive factor for applying the simplification is the transfer of the right to dispose of the goods. Physical possession is not required; what matters is the legal ability to dispose of the goods, for example, by reselling them. However, the simplification rule does not apply if the taxable person knew or should have known that the transaction was part of VAT fraud committed within a supply chain.

4 Consequences for the practice

There are few General Court rulings since the jurisdiction shift at EU level. This judgment, however, is significant, particularly for the German tax administration. It clearly rejects the interpretation in sec. 25b para. 2 of the German Administrative VAT Guidelines. Currently, the German tax authority denies the application of a triangular transaction if it does not involve the last three parties in the chain. As a result, purchasers of the supply of goods to which the transport is assigned to, who appear elsewhere in the chain under a German VAT-ID, face acquisition taxation in Germany according to Art. 41 EU VAT Directive. This taxation is only reversed if the taxable person proves that the acquisition was taxed in the destination country. This regularly results in at least interest charges and an increased administrative burden. In some cases, it can lead to a permanent tax burden if among others the destination Member State recognises the triangular transaction and does not allow registration for B. In such cases, B cannot provide proof of taxation due to the lack of registration. Affected taxable persons should challenge non-final tax and interest assessments.

The General Court states that the simplification rule does not apply if the taxable person knew or should have known that the transaction was part of a VAT fraud within the supply chain. In such cases, acquisition taxation applies because the principle of neutrality is violated. In addition to reviewing business partners (e.g., within a TCMS), the importance of submitting accurate EC Sales Lists is highlighted. Taxable persons should review their processes accordingly.

Contact