1. Background

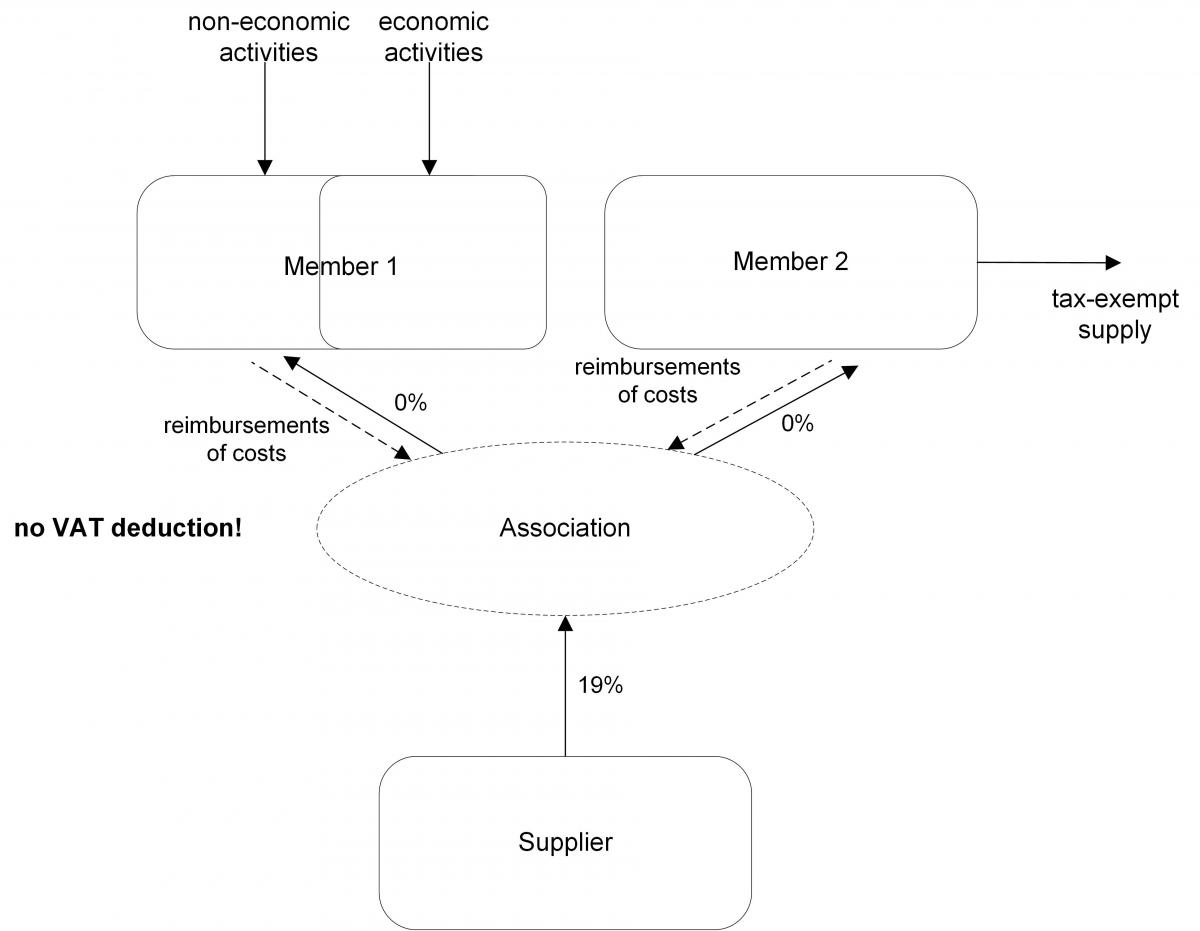

It has been less than five months since the ECJ made its decision in the case Commission/Luxembourg (see KMLZ-Newsletter 12/2017). There, the ECJ stated that, in relation to Art. 132 letter f VAT Directive, the particular association had to be a separate taxpayer, different from its members. This association must also be independent, which is to be understood as a rejection of transparent associations without own legal personality. The ECJ also considered it harmless if the members of the association also carried out taxable activities, i.e. mixed output transactions. However, the court held that the association would benefit from the exemption only if those services were provided directly for the purpose of the activities of those members who were exempted from taxation or with respect to which the members were not taxable persons. With this judgment, a start was made to fill the VAT exemption, pursuant to Art. 132 letter f VAT Directive, with life.

Three other proceedings were then pending which suggested that the ECJ should also comment on the other elements of Art. 132 letter f VAT Directive.

2. Judgments of the ECJ

In its three judgments of 21 September 2017, the ECJ found in the legal cases C-616/15 (Commission/Germany), C-326/15 (DNB Banka) and C-605/15 (Aviva) that solely non-profit-making activities fall within the scope of Art. 132 letter f VAT Directive. The ECJ offered no further explanation as regards other elements. It also found that banks and insurance companies do not benefit from the VAT exemption.

Even if the ECJ does not explicitly say so, it is indeed a change to the case law. In the case of Taksatorringen, the ECJ actually applied a VAT exemption to insurance services, despite the VAT exemption ultimately failing due to the risk of distortions of competition. Moreover, the ECJ has previously expressed its opinion on the meaning of the heading of Chapter 2 under Title IX. As a result, it came as some surprise that the ECJ would limit the exemption of cost sharing associations to non-profit making activities.

3. Impact on the practice

Germany has only implemented the Union law VAT exemption regulation in a very limited way for so-called cost sharing associations in sec. 4 no. 14 letter d German VAT Act. It therefore now remains for the Federal Republic of Germany to extend the VAT exemption regulation afforded by sec. 4 no. 14 letter d German VAT Act to all non-profit-making activities within the meaning of Art. 132 VAT Directive.

This is particularly interesting for cooperation if the association´s services can be invoiced to the member which is not entitled to input VAT deduction without VAT.

Until such time as the legislator adapts the VAT law, taxpayers can refer to the direct application of Article 132 letter f VAT Directive. The national case law has already allowed this in some instances.

The national legislature would therefore do well not to restrict the VAT exemption of non-profit making sharing associations for the benefit of the general public. It is often non-profit organizations that are condemned to co-operate in order to save costs. And in the end, this saving ultimately finds its way back to the general public.

Contact